What a brutal six months it’s been for Conagra. The stock has dropped 20.3% and now trades at $21.60, rattling many shareholders. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Is now the time to buy Conagra, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think Conagra Will Underperform?

Despite the more favorable entry price, we don't have much confidence in Conagra. Here are three reasons why CAG doesn't excite us and a stock we'd rather own.

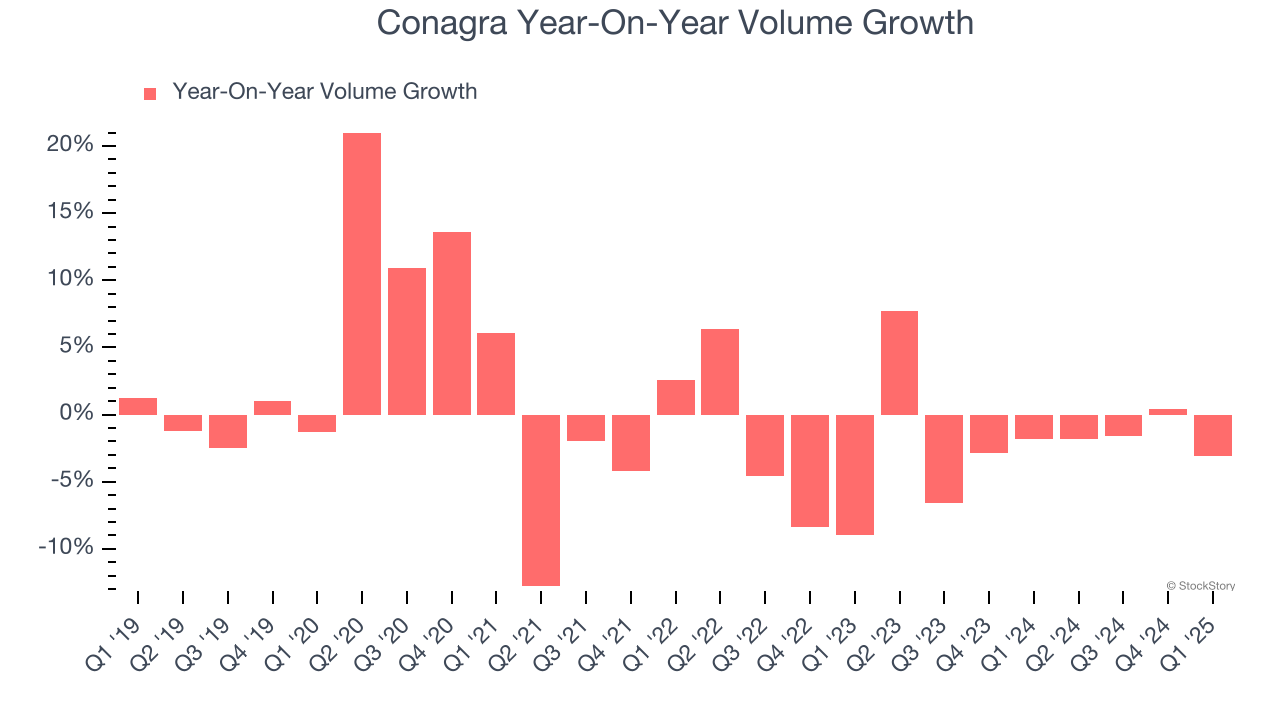

1. Demand Slipping as Sales Volumes Decline

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

Conagra’s average quarterly sales volumes have shrunk by 1.2% over the last two years. This decrease isn’t ideal because the quantity demanded for consumer staples products is typically stable.

2. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Conagra’s revenue to drop by 2.4%, a decrease from This projection is underwhelming and suggests its products will face some demand challenges.

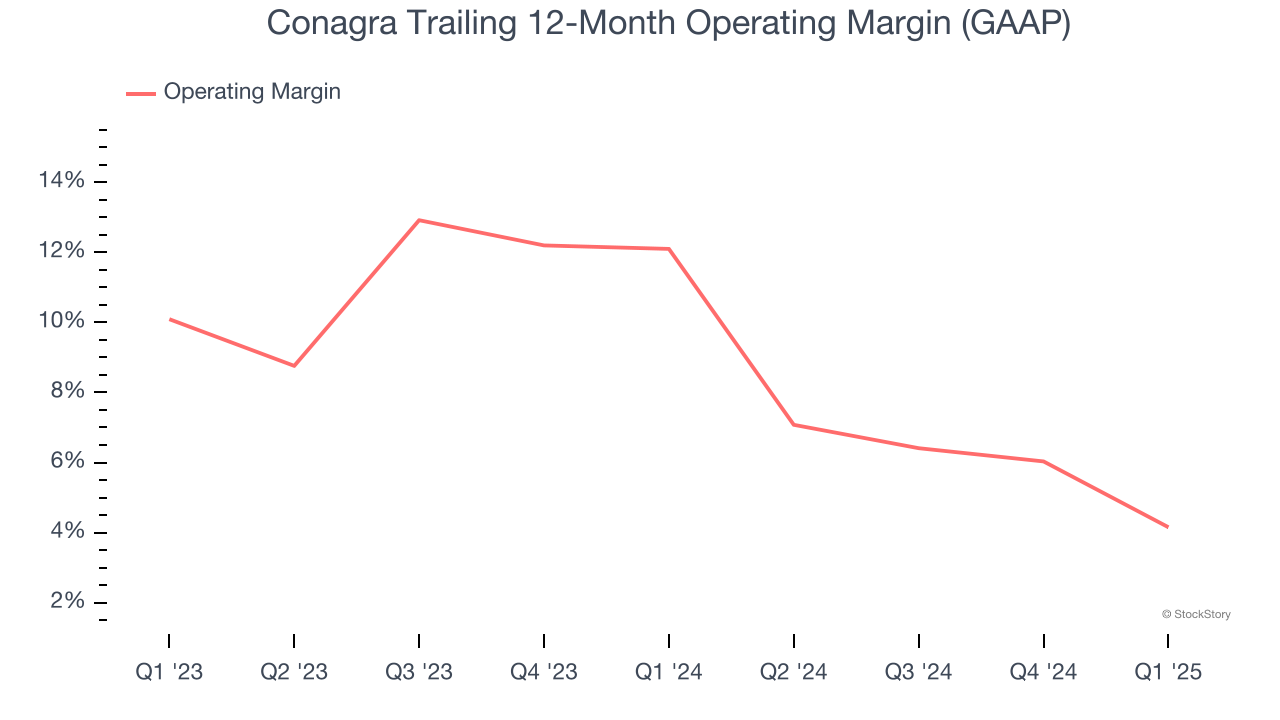

3. Shrinking Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Analyzing the trend in its profitability, Conagra’s operating margin decreased by 7.9 percentage points over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its operating margin for the trailing 12 months was 4.2%.

Final Judgment

We cheer for all companies serving everyday consumers, but in the case of Conagra, we’ll be cheering from the sidelines. After the recent drawdown, the stock trades at 8.8× forward P/E (or $21.60 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better investments elsewhere. We’d suggest looking at one of our all-time favorite software stocks.

Stocks We Would Buy Instead of Conagra

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.