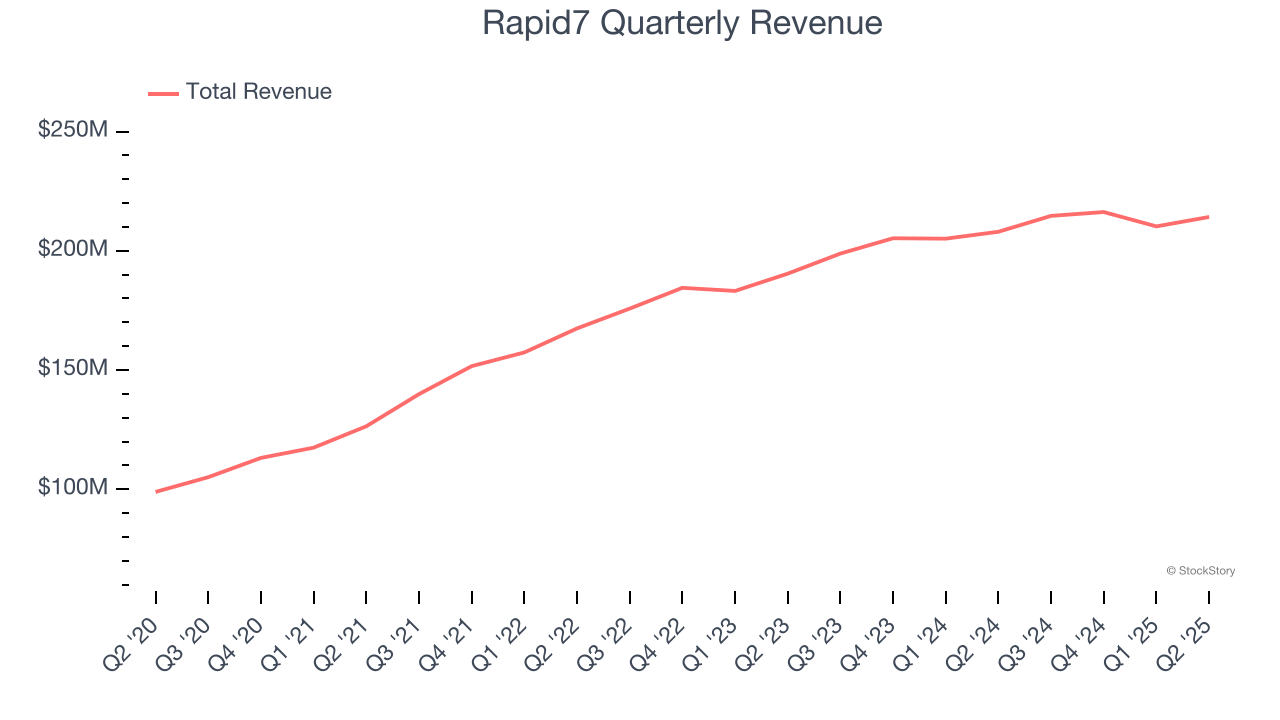

Cybersecurity software maker Rapid7 (NASDAQ:RPD) reported Q2 CY2025 results beating Wall Street’s revenue expectations, with sales up 3% year on year to $214.2 million. The company expects next quarter’s revenue to be around $216 million, close to analysts’ estimates. Its non-GAAP profit of $0.58 per share was 30.8% above analysts’ consensus estimates.

Is now the time to buy Rapid7? Find out by accessing our full research report, it’s free.

Rapid7 (RPD) Q2 CY2025 Highlights:

- Revenue: $214.2 million vs analyst estimates of $212 million (3% year-on-year growth, 1.1% beat)

- Adjusted EPS: $0.58 vs analyst estimates of $0.44 (30.8% beat)

- Adjusted Operating Income: $36.35 million vs analyst estimates of $30.87 million (17% margin, 17.7% beat)

- The company reconfirmed its revenue guidance for the full year of $858 million at the midpoint

- Management raised its full-year Adjusted EPS guidance to $1.96 at the midpoint, a 6.5% increase

- Operating Margin: 1.6%, in line with the same quarter last year

- Free Cash Flow Margin: 19.7%, up from 11.7% in the previous quarter

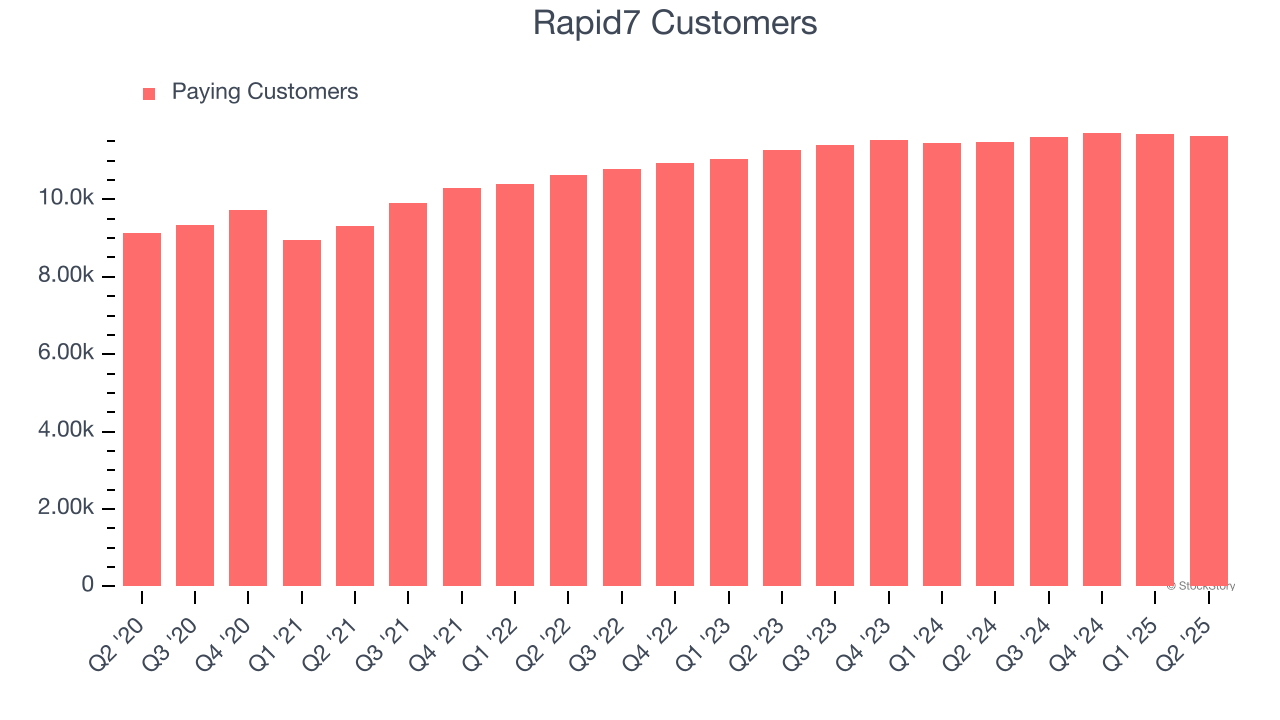

- Customers: 11,643, down from 11,685 in the previous quarter

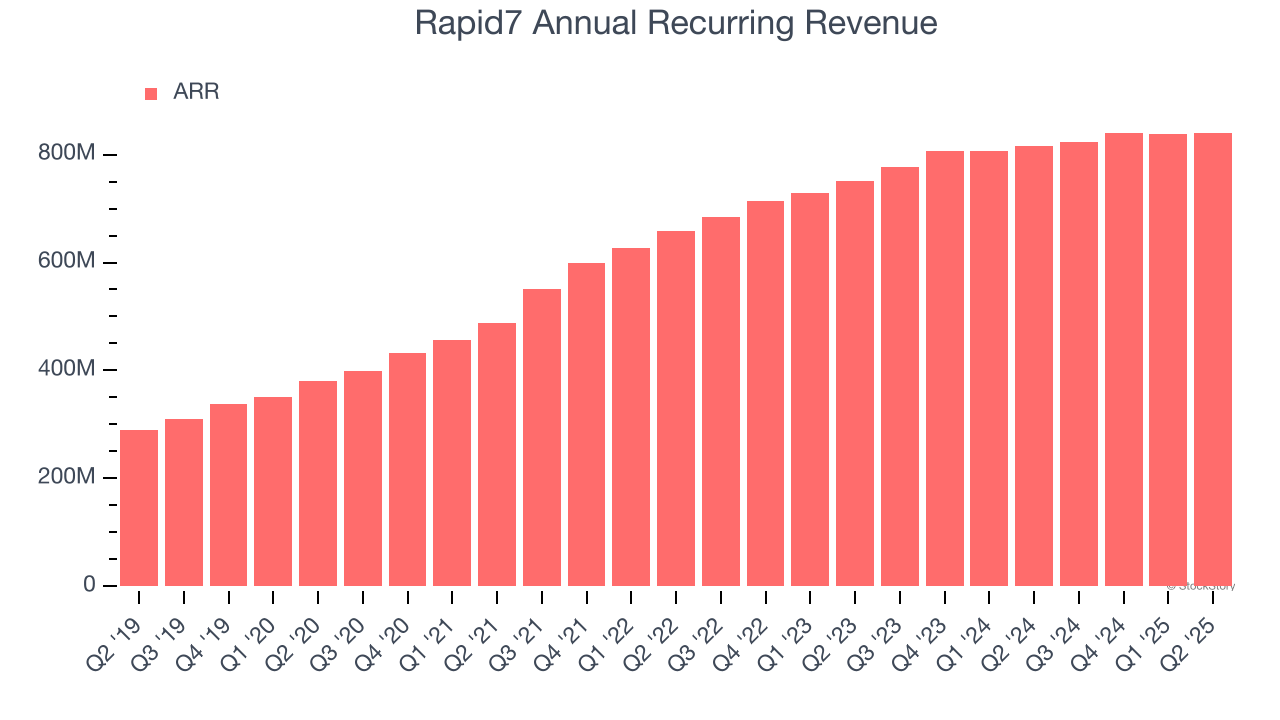

- Annual Recurring Revenue: $840.6 million at quarter end, up 3.1% year on year

- Market Capitalization: $1.28 billion

“Our Detection and Response business remains a consistent growth engine, and we are encouraged by growing customer interest in our Command Platform strategy,” said Corey Thomas, CEO of Rapid7.

Company Overview

Founded in 2000 with the idea that network security comes before endpoint security, Rapid7 (NASDAQ:RPD) provides software as a service that helps companies understand where they are exposed to cyber security risks, quickly detect breaches and respond to them.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last three years, Rapid7 grew its sales at a 11.5% compounded annual growth rate. Although this growth is acceptable on an absolute basis, it fell short of our standards for the software sector, which enjoys a number of secular tailwinds.

This quarter, Rapid7 reported modest year-on-year revenue growth of 3% but beat Wall Street’s estimates by 1.1%. Company management is currently guiding for flat sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 2.3% over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and indicates its products and services will face some demand challenges.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Annual Recurring Revenue

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Rapid7’s ARR came in at $840.6 million in Q2, and over the last four quarters, its growth was underwhelming as it averaged 4.2% year-on-year increases. This performance mirrored its total sales and suggests that increasing competition is causing challenges in securing longer-term commitments.

Customer Base

Rapid7 reported 11,643 customers at the end of the quarter, a sequential decrease of 42. That’s better than last quarter but a bit below what we’ve seen over the previous year. This indicates the company is optimizing its go-to-market strategy to reinvigorate growth.

Key Takeaways from Rapid7’s Q2 Results

We were impressed by how significantly Rapid7 blew past analysts’ EBITDA expectations this quarter. We were also glad its full-year EPS guidance trumped Wall Street’s estimates. On the other hand, its EPS guidance for next quarter missed and its revenue guidance for next quarter was in line with Wall Street’s estimates. Overall, this print was mixed but still had some key positives. The stock remained flat at $19.92 immediately following the results.

So do we think Rapid7 is an attractive buy at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.