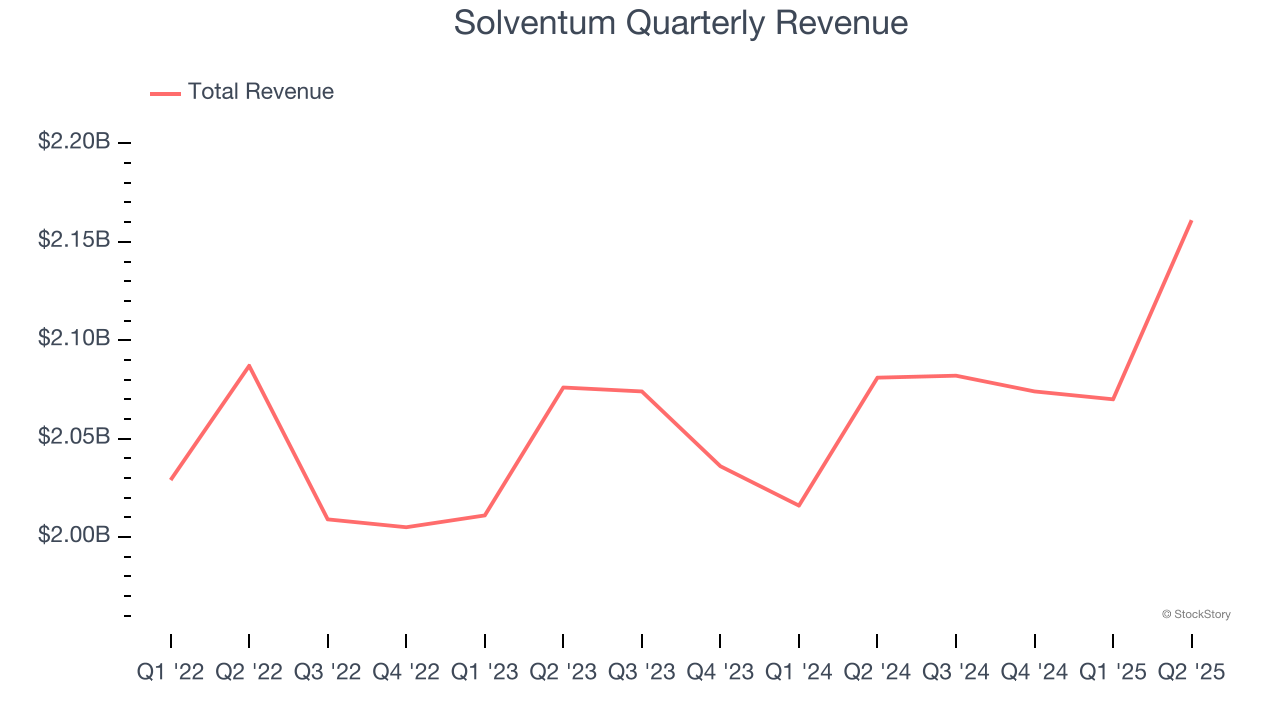

Healthcare solutions provider Solventum (NYSE:SOLV) beat Wall Street’s revenue expectations in Q2 CY2025, with sales up 3.8% year on year to $2.16 billion. Its non-GAAP profit of $1.69 per share was 16.3% above analysts’ consensus estimates.

Is now the time to buy Solventum? Find out by accessing our full research report, it’s free.

Solventum (SOLV) Q2 CY2025 Highlights:

- Revenue: $2.16 billion vs analyst estimates of $2.12 billion (3.8% year-on-year growth, 1.9% beat)

- Adjusted EPS: $1.69 vs analyst estimates of $1.45 (16.3% beat)

- Adjusted EBITDA: $370 million vs analyst estimates of $533.7 million (17.1% margin, 30.7% miss)

- Management reiterated its full-year Adjusted EPS guidance of $5.55 at the midpoint

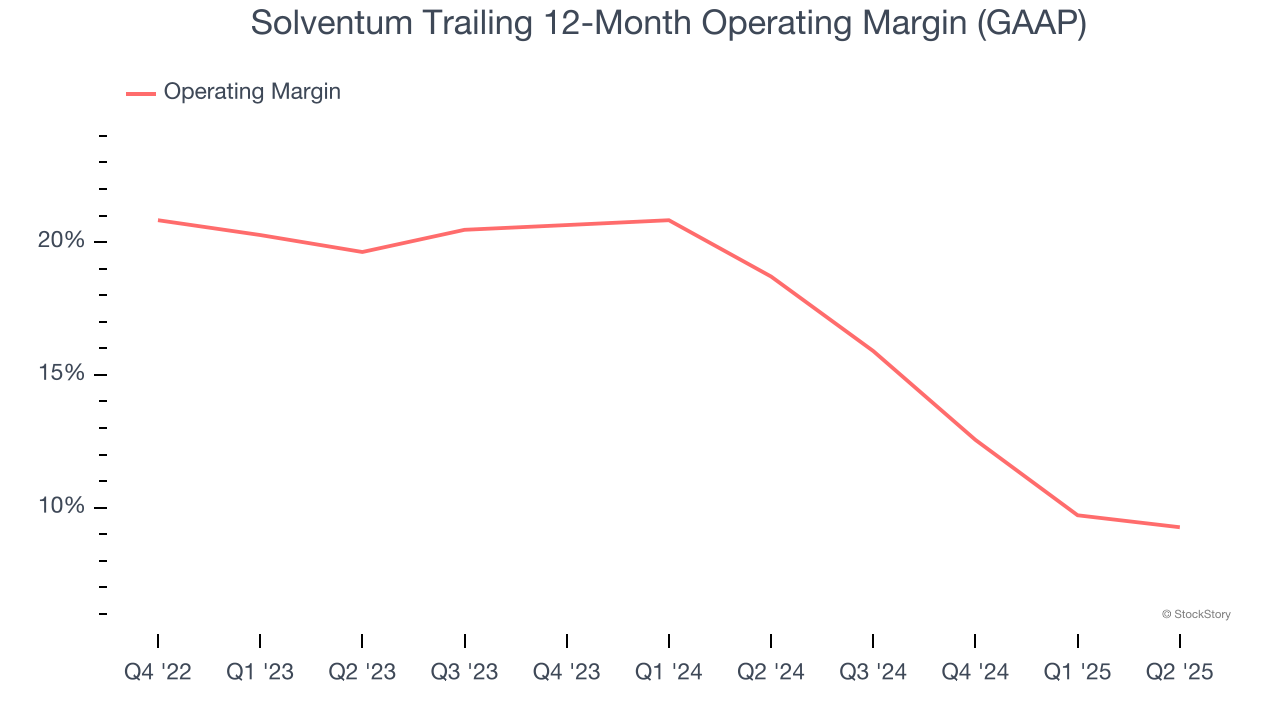

- Operating Margin: 9.9%, down from 11.7% in the same quarter last year

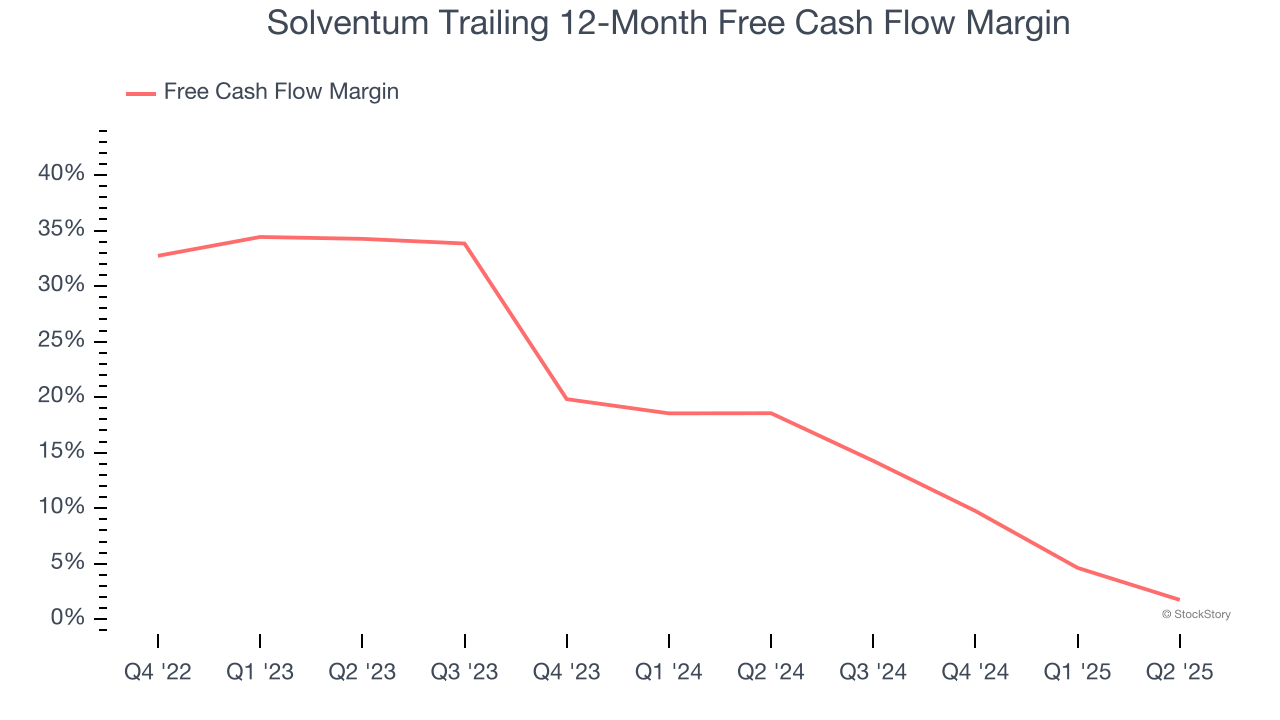

- Free Cash Flow Margin: 2.7%, down from 14.3% in the same quarter last year

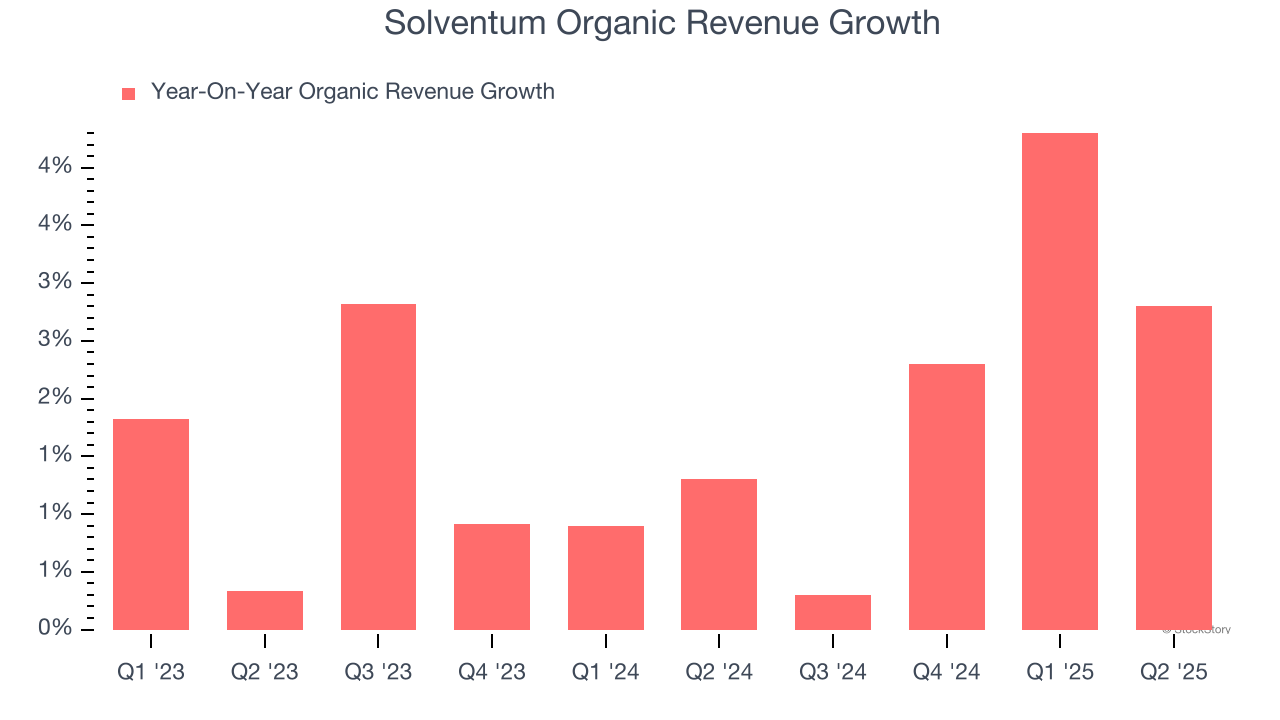

- Organic Revenue rose 2.8% year on year (1.3% in the same quarter last year)

- Market Capitalization: $12.56 billion

"Our solid second quarter fiscal year 2025 results mark five consecutive quarters of positive sales volume growth since implementing our transformation strategy," said Bryan Hanson, CEO of Solventum.

Company Overview

Founded in 1985, Solventum (NYSE:SOLV) develops, manufactures, and commercializes a portfolio of healthcare products and services addressing critical customer and therapeutic patient needs.

Revenue Growth

A company’s top-line performance is one signal of its overall business quality. Strong growth can indicate it’s riding a successful new product or emerging trend. Solventum’s annualized revenue growth rate of 1.7% over the last two years was tepid for a healthcare business.

We can dig further into the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Solventum’s organic revenue averaged 2% year-on-year growth. Because this number aligns with its two-year revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Solventum reported modest year-on-year revenue growth of 3.8% but beat Wall Street’s estimates by 1.9%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a slight deceleration versus the last two years. This projection is underwhelming and suggests its products and services will see some demand headwinds.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

Solventum has managed its cost base well over the last four years. It demonstrated solid profitability for a healthcare business, producing an average operating margin of 16.6%.

Looking at the trend in its profitability, Solventum’s operating margin decreased by 12.9 percentage points over the last four years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 10.4 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

In Q2, Solventum generated an operating margin profit margin of 9.9%, down 1.8 percentage points year on year. This reduction is quite minuscule and indicates the company’s overall cost structure has been relatively stable.

Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Solventum has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 17.6% over the last four years, quite impressive for a healthcare business.

Taking a step back, we can see that Solventum’s margin dropped by 15.7 percentage points during that time. If its declines continue, it could signal increasing investment needs and capital intensity.

Solventum’s free cash flow clocked in at $59 million in Q2, equivalent to a 2.7% margin. The company’s cash profitability regressed as it was 11.5 percentage points lower than in the same quarter last year, suggesting its historical struggles have dragged on.

Key Takeaways from Solventum’s Q2 Results

We enjoyed seeing Solventum beat analysts’ EPS expectations this quarter. We were also happy its organic revenue narrowly outperformed Wall Street’s estimates. On the other hand, its full-year EPS guidance slightly missed. Overall, this print had some key positives. The stock remained flat at $71.95 immediately following the results.

Big picture, is Solventum a buy here and now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.