Over the last six months, Universal Display’s shares have sunk to $141.50, producing a disappointing 8.3% loss - a stark contrast to the S&P 500’s 16.8% gain. This might have investors contemplating their next move.

Given the weaker price action, is now a good time to buy OLED? Find out in our full research report, it’s free.

Why Does OLED Stock Spark Debate?

Serving major consumer electronics manufacturers, Universal Display (NASDAQ:OLED) is a provider of organic light emitting diode (OLED) technologies used in display and lighting applications.

Two Positive Attributes:

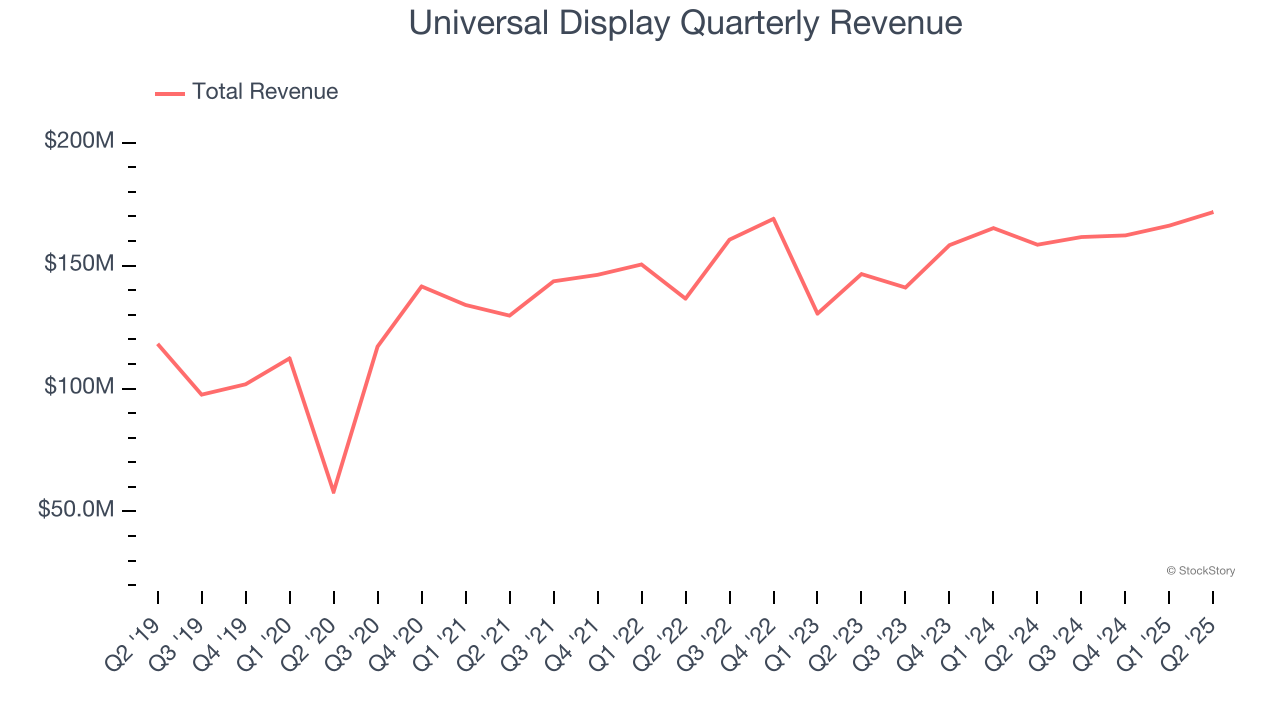

1. Long-Term Revenue Growth Shows Strong Momentum

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, Universal Display’s sales grew at a solid 12.4% compounded annual growth rate over the last five years. Its growth surpassed the average semiconductor company and shows its offerings resonate with customers. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

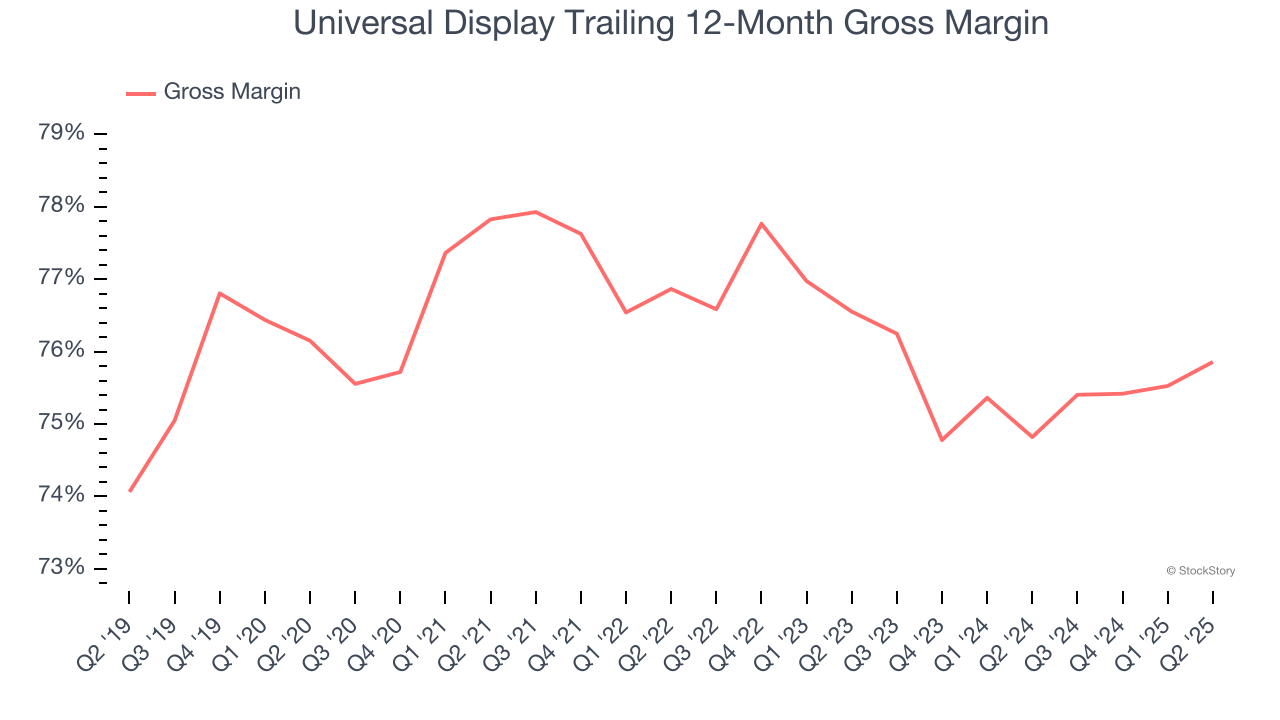

2. Elite Gross Margin Powers Best-In-Class Business Model

Gross profit margin is a key metric to track because it shows how much money a semiconductor company gets to keep after paying for its raw materials, manufacturing, and other input costs.

Universal Display’s gross margin is one of the best in the semiconductor sector, and its strong pricing power is a direct result of its differentiated products and technological expertise. As you can see below, it averaged an elite 75.4% gross margin over the last two years. That means Universal Display only paid its suppliers $24.64 for every $100 in revenue.

One Reason to be Careful:

Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Universal Display’s revenue to rise by 4.3%, close to its 12.4% annualized growth for the past five years. This projection doesn't excite us and indicates its newer products and services will not lead to better top-line performance yet. At least the company is tracking well in other measures of financial health.

Final Judgment

Universal Display has huge potential even though it has some open questions. With the recent decline, the stock trades at 30× forward EV-to-EBITDA (or $141.50 per share). Is now the right time to buy? See for yourself in our comprehensive research report, it’s free.

Stocks We Like Even More Than Universal Display

When Trump unveiled his aggressive tariff plan in April 2025, markets tanked as investors feared a full-blown trade war. But those who panicked and sold missed the subsequent rebound that’s already erased most losses.

Don’t let fear keep you from great opportunities and take a look at Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.